Contents

Content

The respective normal account balances of Sales, Sales Returns and Allowances, and Sales Discounts are a. Thus, the total balance of current assets will not remain the same. ABC Inc sold goods worth $1,000 to XYZ Inc on January 1, 2019, on which 10% tax is applicable.

- On the balance sheet, it is recorded as accounts receivable signifying that the amount is owed to the company.

- Little Electrode, Inc. purchased this monitor from the manufacturer for $750 three months ago.

- Sales credit journal entry is vital for companies that sell their goods on credit.

- A credit to accounts receivable decreases the account.

- A credit sale is an agreement between a buyer and seller where the buyer can purchase goods or services on credit, meaning the buyer does not have to make payment immediately but rather at a later date.

- It is made using the double-entry bookkeeping method.

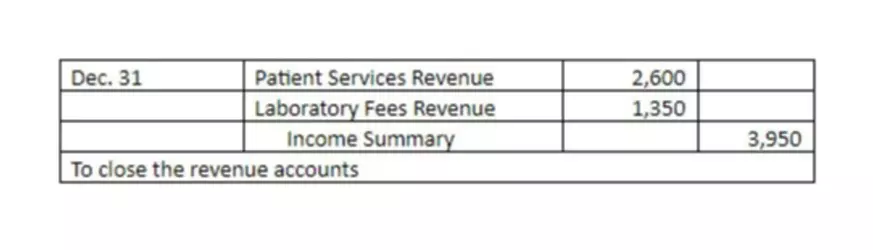

A How to Record a Credit Sale sets up an allowance for doubtful accounts to place the expense of uncollectible accounts in the same accounting period as.. We have increased our cash and revenue, and also recognised that to generate that revenue – the business had to use some resources.

Sales journal entry definition

Mostly Customers prefer to buy goods on credit than in cash. Once the cash is received, the account receivable created is reversed in the books of accounts of the seller. The record can give insight into periods of high patronage and those of low patronage. Hence, it can be used to gauge the business’s performance over time. It aids the company in keeping track of all amounts owed to them by customers and further makes follow-up for money retrieval easier.

- Credit sales represent sales not paid immediately at the date of invoice.

- Later, when the customer does pay, you can reverse the entry and decrease your Accounts Receivable account and increase your Cash account.

- Either the ending or average A/R balance can be used in the formula, but the difference are marginal — unless there is a clear shift in the A/R balances due to operational changes.

- But what happens if at the end of the year, some paper or pens or toilet paper haven’t been used?

- In addition, you may have noticed that most of our prior examples are related to businesses that provide services rather than goods.

An increase in credit sales shows that more customers are taking advantage of the credit sales that are offered by a company. Companies are careful when extending credit to customers since a failure to pay the amount owed adds to the company’s bad debt. Bad debt refers to all amounts owed to the company by its clients which are considered irrecoverable. Sales are a part of everyday business, they can either be made in cash or credit. In a dynamic environment, credit sales are promoted to keep up with the cutting edge competition. Accounting and journal entry for credit sales include 2 accounts, debtor and sales.

How to Calculate Sales Returns in a General Ledger

Credit sales can be used to more easily acquire new customers. Offering credit can attract new customers to purchase from the company. Expense accounts record what a company has spent money on, like payroll or inventory.

We have reduced our prepaid asset and increased our expenses . The business would record this transaction at the end of every month until the prepaid asset is reduced to a balance of $0. In the above example, the business has purchased paper and recorded it as an asset. Theoretically, this is correct – the paper is an asset.

Credit Terms with Discounts

Balance Sheet Of The CompanyA balance sheet is one of the financial statements of a company that presents the shareholders’ equity, liabilities, and assets of the company at a specific point in time. It is based on the accounting equation that states that the sum of the total liabilities and the owner’s capital equals the total assets of the company.

The specific steps for each type of sale are then separately discussed under the appropriate heading below. A major portion of wholesale and retail sales in the United States is on credit. To illustrate the meaning of net, assume that Gem Merchandise Co. sells $1,000 of goods to a customer. Upon receiving the goods the customer finds that $100 of the goods are not acceptable. The customer contacts Gem and is instructed to return the unacceptable goods. This means that Gem’s net sale ends up being $900; the customer’s net purchase will also be $900 ($1,000 minus the $100 returned).

Recognising when we use inventory

In that case, the https://www.bookstime.com/s may not show up as transactions until the bookkeeper receives the credit card statement, which may be in the next accounting period. If the amounts are immaterial according to the company’s subjective assessment of that term, recording June expenses in July may be acceptable. However, the proper way to record the expenses would be to accrue them to the proper period. Let us have a look at how the various credit sales journal entries are actually recorded during the course of the daily operations of companies. When companies offer goods or services on credit, they often do so with stipulated conditions for the payment of the amount owed; these conditions are referred to as credit terms.

- It gives them the required time to collect money & make the payment.

- Unlike petty cash, which is usually a fairly small amount of money, credit card charges can add up quickly and get out of control if not carefully monitored.

- This is mostly true for companies that sell expensive items.

- Liabilities, equity, and revenue are increased by credits and decreased by debits.

The credit terms of purchases are usually indicated on the invoice of the purchase. It usually indicates when the amount owed is due for payment, any sales discount for the purchase as well as any applicable late payment fees or interest. What is the journal entry to record a credit sale? The average collection period is calculated by dividing total annual credit sales by half the sum of the balance of starting receivables and the balance of ending receivables. The average collection period, as well as the receivables turnover ratio, offer useful insight into assessing the company’s cash flow and overall liquidity. If the selected customer has a sales order that is open then the window displays the Apply to Sales Order No. tab rather than the Apply to Sales tab. Here, in the drop down box next to Apply to Sales Order No., select the sales order number applicable to the sale.